Why “Recession” Headlines Might Be Good News for Your Mortgage

You’ve probably seen the headlines this week: Canada has entered a technical recession. It sounds alarming. But before you worry, let me walk you through what actually happened — because for anyone with a mortgage coming up for renewal, or anyone thinking about buying, this news is far less scary than the headline suggests. In some ways, it’s quietly encouraging.

First, what “technical recession” really means

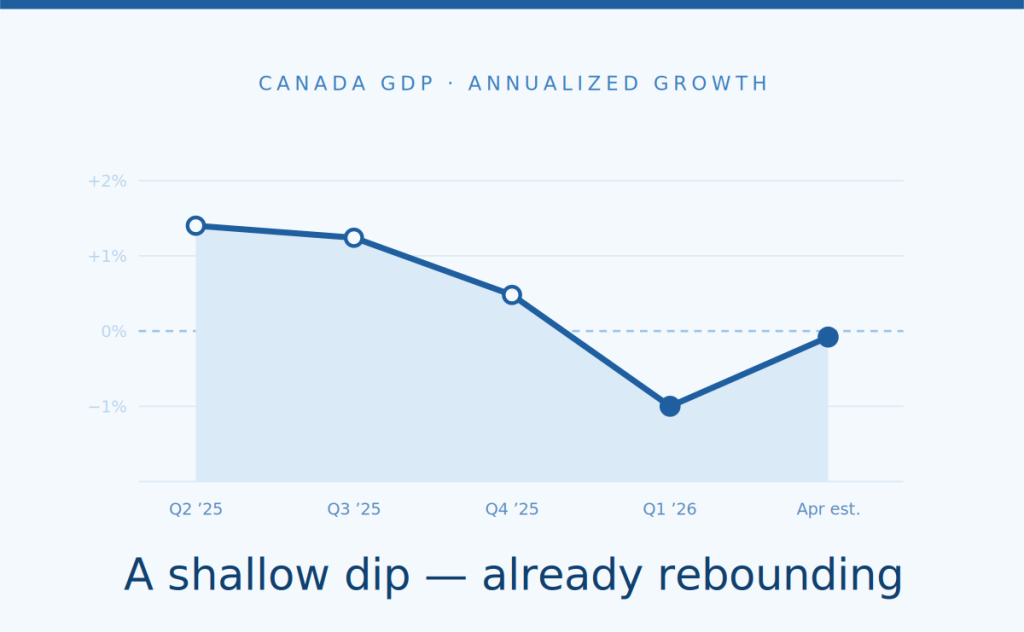

This morning, Statistics Canada reported the economy shrank by 0.1% in the first quarter of 2026, on the heels of a 1% decline at the end of last year. Two small declines in a row is the textbook definition of a “technical recession.”

But here’s the part the headlines skip: when you measure the economy per person, it actually grew by 0.2%. The overall number dipped mostly because Canada’s population shrank slightly — not because families suddenly stopped spending or working. Household spending actually rose. In plain terms, this is a stall, not a crash.

Why a stalling economy can mean better mortgage rates

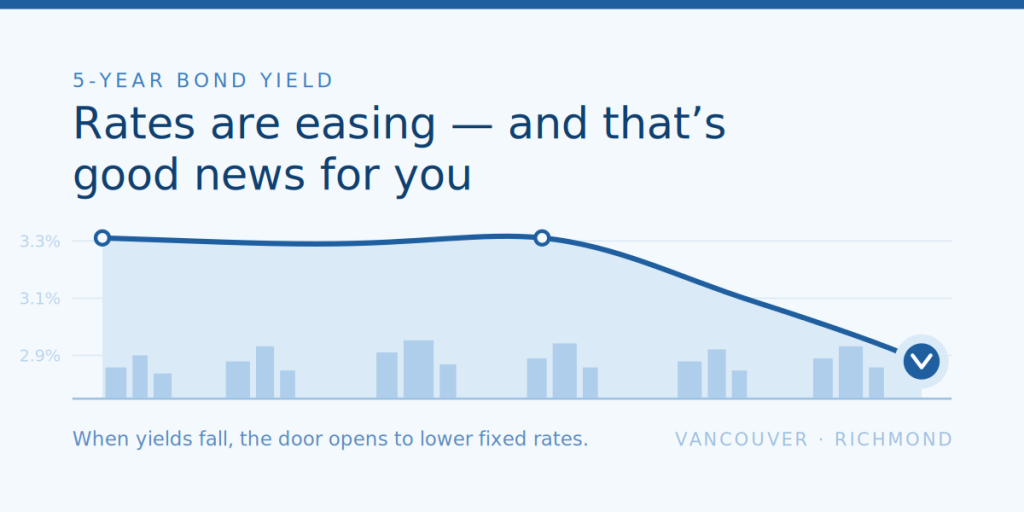

Here’s the connection most people miss. Fixed mortgage rates in Canada don’t follow the Bank of Canada directly — they follow government bond yields. When the economy looks soft, investors pile into the safety of Canadian bonds, pushing yields down. And when bond yields fall, lenders can offer lower fixed rates.

That’s exactly what’s been happening. The 5-year Government of Canada bond yield — the single most important number for 5-year fixed mortgages — has drifted lower over the past month. The yield on the Canada 5-year bond eased to around 3.11% in late May, down roughly 0.15 points over the month. That downward drift is the kind of quiet tailwind that can translate into better fixed-rate offers.

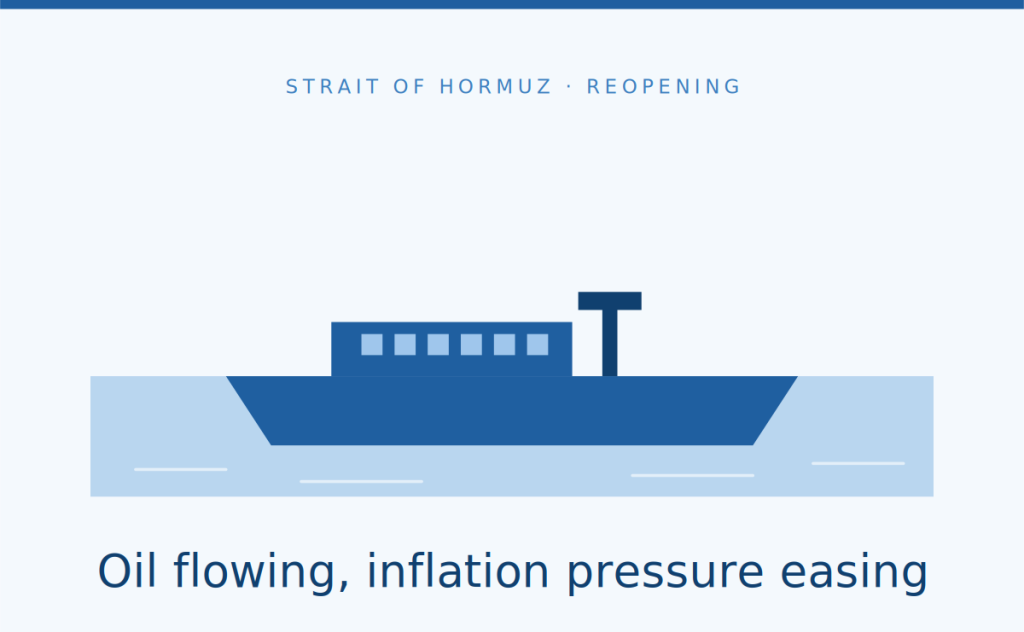

For months, one of the biggest threats to lower rates was the war in Iran. When Iran closed the Strait of Hormuz — the narrow waterway that carries a huge share of the world’s oil — energy prices spiked, and higher oil prices tend to feed inflation. Stubborn inflation is the one thing that keeps interest rates high.

The good news: that conflict is now de-escalating. The United States and Iran have built a framework to extend the ceasefire and reopen the Strait of Hormuz, with traffic expected to return to pre-war conditions within about 30 days. President Trump has said a deal to reopen the Strait is “largely negotiated.” As that waterway reopens and oil flows normally again, one of the major upward pressures on inflation begins to fade.

Markets are calming down, too

You can see the relief in the “fear gauge.” The VIX — Wall Street’s measure of market anxiety — has fallen to around 15.7, well down from the high-20s back in March. Lower fear means calmer markets, and calmer markets tend to keep bond yields steady or lower. All of this points in the same direction: less pressure pushing rates up.

What the Bank of Canada is likely to do on June 10

Put it together — a soft economy, cooling inflation pressure, a de-escalating war, and calmer markets — and you get a Bank of Canada that has good reason to stay put. The Bank has already held its key rate at 2.25% three meetings in a row, and the most likely outcome on June 10 is a fourth hold.

A hold is not bad news. It means stability. It means the surprises that whipsaw rates are, for now, off the table — and the underlying trend in bond yields is gently downward.

What this means for you

None of this is about chasing the lowest possible rate on a given day. It’s about building a plan that gives you peace of mind regardless of which way the headlines turn. That’s my job — and I’m watching these numbers daily so you don’t have to.

A quick, honest note: rates move daily and nobody can promise where they’ll land. The trends above are encouraging, but they’re trends, not guarantees. The value is in having a strategy ready to act on them.

![]() Copyright © 2026 Michael Friedman. All Rights Reserved.

Copyright © 2026 Michael Friedman. All Rights Reserved.